Like any good detective, we follow the paper trail when the story does not quite add up. The AI boom is easy to admire from a distance, but harder to make sense of up close. So we follow the money trail it leaves behind.

The point is not just to ask who is winning. It is to understand what is really holding the boom together in the first place.

Over the past couple of years, AI has gone from a niche technology to something that has changed the way we think, work, make decisions and execute. Adoption is no longer optional. It is already embedded in everyday life.

Capital markets have noticed.

Nvidia’s stock, a company that once sold graphics chips to gamers, climbed from 16.75 dollars in mid December 2022 to 222.75 dollars by mid May 2026, a 100%+ CAGR over several years in a company already worth hundreds of billions.

And Nvidia is hardly alone. Across the market, companies plugged into building AI systems have been valued higher. The closer you are to the AI backbone, the better your stock seems to do.

At first glance, the story sounds simple. AI is the future. Infrastructure is how you get there. So buy the infra companies. If this is where the growth is, why not just own it?

To see why that explanation may be too neat, it helps to zoom out and look at the full stack.

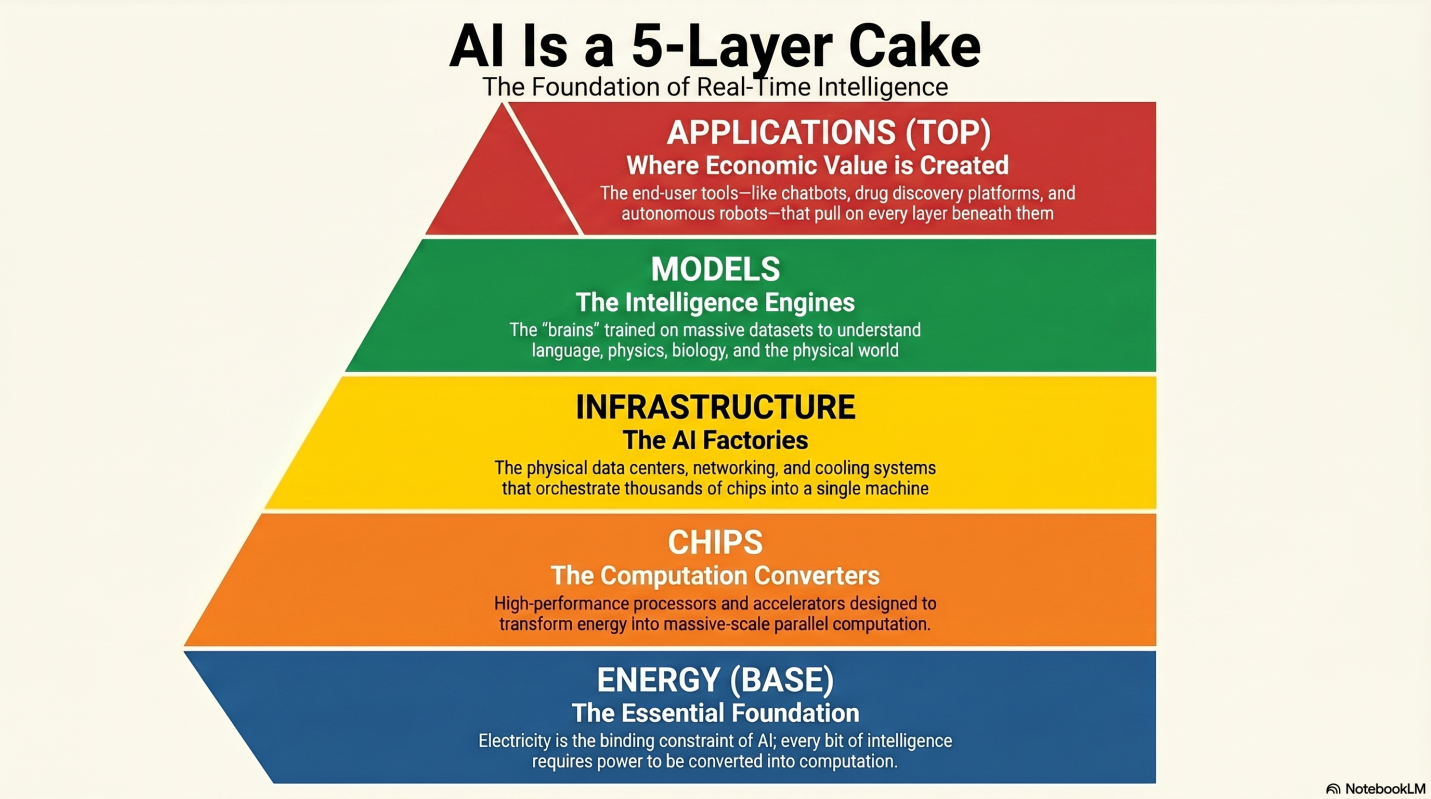

Nvidia’s CEO Jensen Huang describes AI as a five layer “cake.”

Each layer rests on the one below it, and value flows upward through the stack.

At the base is power. Without cheap, reliable electricity, nothing else works. On top of that sit the chips, GPUs and accelerators that perform the computation. Those chips live inside a global web of data centres, networks and storage that form the infrastructure layer. Above that are the AI models, the “brains” trained on massive datasets. At the very top are the applications, copilots, chatbots, productivity tools and industry specific systems where most of the eventual end user revenue is supposed to appear.

Right now, the economic centre for this cake, is not at the top of the cake. The bulk of the capital and the most dramatic share price moves are concentrated in the middle, in the chips and infrastructure that feed them.

Models are expensive to train, but do not yet generate enough cash. Applications are still early in their adoption curve. The result is a world where the layers that enable AI may be earning more, and being valued more highly, than the layers that actually sell AI to customers.

This note is about that middle of the stack, the part of the cake where chips, cloud and data centres meet, and about the financial structure that sits behind it.

Hence, the more prudent question, in our view, is not where the growth is showing up, but how it is being created. Where is the money actually coming from? Where does it end up? And does it quietly circle back to the same few companies that began the process?

How Does the AI Machine Run

To see the machine at work, it helps to peel back the top of the cake and look at what an AI lab actually needs to function.

Take the AI labs at the model layer, OpenAI, Anthropic and their peers. Their biggest bills are not office rent or staff. They are infrastructure.

At a basic physical level, these AI labs rely on three building blocks.

- Cloud infrastructure, remote servers used to train and run models.

- GPUs, specialised chips that handle the heavy computational workload.

- Data centres, the physical facilities that house and power large clusters of these GPUs.

This infrastructure is expensive. Even at a moderate scale, running advanced models can cost 2-5 million USD per month in compute tasks alone. Training a new flagship model pushes those numbers significantly higher.

The labs do bring in revenue from consumers and enterprises, but not nearly enough to cover the capital expenditure required to keep building bigger, more capable systems. OpenAI has been reported to be losing ~4 billion USD a year, whereas Anthropic at ~2 billion USD. These are, by design, loss making for the time being. They have the capability, but are constrained by capital. On their own, they do not generate the cash flows to sustain the infrastructure they depend on.

It is crucial to distinguish the three essential actors in this story.

- Hyperscalers, mainly Microsoft, Amazon and Google, who require chips with exceptional computing power and operate data-centres with the help of these chips. These data-centres in turn help train AI models and execute the prompts we give to said model, like ChatGPT.

- Chip/GPU providers, primarily Nvidia and AMD, design and sell the GPUs and accelerators. Who in turn require huge amounts of specialized chips from TSMC, and high-bandwidth-memory from Samsung, SK Hynix, and Micron.

- AI labs such as OpenAI and Anthropic sit one level up, building the models that run on the above mentioned infrastructure.

They are tightly linked, but not interchangeable. Each plays a different role in how capital and revenue move through the system.

At the top of the cake sit the applications that are meant to pay for all of this. Copilots, chatbots, productivity tools, vertical solutions. The reality today is that this application layer is still small compared with the size of the bet being placed underneath it. This setting will persist until end users start generating the kind of revenue needed to sustain the AI infrastructure’s capex requirements.

That is where the largest technology companies in the world walk in, not just as suppliers, but as investors. The obvious question then shifts. What exactly are Microsoft, Amazon, Google and Nvidia getting in return for pouring tens of billions into these labs? Haven’t they already won the last decade?

Central Layers of the Cake

At its simplest, the structure works as follows.

A hyperscaler writes a cheque into an AI lab and takes an ownership stake. The lab uses that capital to sign long dated commitments for cloud and/or compute, often with the same company that invested. These contracts then turn into high-margin revenue for the investors, who in this setting are also the providers of the ecosystem.

That revenue, in turn, lifts the AI lab’s valuation while delivering high-margin revenue that strengthens the hyperscaler’s balance sheet.

Contracted demand makes the lab’s future cash flows look more reliable, which nudges investors to pay higher multiples and makes lenders more comfortable extending capital. Raising the next round becomes easier when the lab can point to booked demand, while the hyperscaler can point to fast-growing, high-margin revenue.

In effect, a significant share of the capital that goes into AI labs loops back into the same small group of firms as infrastructure revenue. The same dollar supports both the asset value of an AI lab and the reported revenue of a listed tech giant, via multi-year contracts.

On a small scale, this would essentially be vendor financing. At today’s scale, it begins to look like an ecosystem wide capital loop.

One Loop, In Full

Microsoft was the first to institutionalize this model.

Over multiple rounds, it has invested more than 13 billion USD into OpenAI. After some restructuring of terms in 2025, Microsoft’s initial investment was valued around 135 billion USD, roughly 27 percent. On paper, that is an astonishing return. But the loop does not end with the valuation increasing.

OpenAI has also committed to purchase roughly 250 billion dollars of Azure cloud services over time. Microsoft is not merely betting on OpenAI’s valuation. It has effectively locked in one of the world’s most important AI applications as a flagship customer of its cloud platform, with demand and revenue contractually anchored years into the future.

Capital flows one way, from Microsoft’s balance sheet into OpenAI. Revenue and an up-lift in the value of Microsoft’s original investment flows back the other way.

What started as a bilateral deal then, now looks like a template.

Nvidia is in discussions to commit up to 100 billion dollars to AI infrastructure projects linked to OpenAI and others. Those same projects could drive hundreds of billions of dollars of GPU and system demand over time. Amazon has built a similar structure around Anthropic, committing capital in return for over 100 billion dollars of planned spend on AWS and Amazon designed chips. Google, along with Microsoft and Nvidia, also appears on both sides of Anthropic’s balance sheet, as an investor and as an infrastructure provider.

Across these arrangements, a pattern emerges. The same small group of firms are funding AI labs, supplying their infrastructure, and anchoring demand with their own capital. Until the top of the cake, the end user applications, can generate enough revenue to pay for the lower layers, this loop is what keeps the system spinning.

Vendor Financing, Hardware and Concentration

In financial terms, what ties these relationships together is vendor financed demand and the way it appears on the balance sheet. Part of the capital that goes into AI labs comes back as long dated, non-cancellable contracts for compute and cloud. Those contracts appear as revenue for cloud providers and chip vendors, with high margins and unusual visibility. The story this tells the market is one of durable growth and locked in demand.

This does not make the revenue fake. The services are real, the chips are real, the workloads exist. But it does raise an important question. How much of this growth is supported by independent end demand, and how much depends on capital continuing to circulate within this small, self-reinforcing system?

The value-addition of AI models takes time to show up. Models are expensive and slow to build, they need to be integrated into real workflows, and the broad based demand at the application layer will likely arrive much later. No one yet knows when that revenue will fully materialise, nor whether the current structure can keep all the layers stacked and stable until AI labs generate enough revenue and profit to fund the constant capex required to upgrade and sustain the ecosystem.

Meanwhile, the physical backbone of AI has its own constraints.

Unlike for traditional software, AI infrastructure is both capital intensive and short lived. High end GPUs deployed in data centres typically have an effective service life of roughly 1-3 years under heavy utilisation. Thermal stress, failure rates and rapid improvements in chip performance make older systems uneconomic relatively quickly.

In practice, most hardware is run hard and replaced frequently, more like a Formula 1 car than a finished highway.

That matters because the same companies that finance the labs are the ones selling this hardware and capacity. When capital flows in, it drives fresh demand for GPUs, servers, networking gear and data centre buildout. As long as the money keeps flowing, vendors like Nvidia can enjoy extremely high levels of demand. If funding slows, or if end market usage fails to scale as expected, the system could be left with a large, rapidly ageing installed base facing a tougher replacement environment.

The supply chain that enables all of this is narrow. Advanced packaging technologies used to make GPUs, are dominated by a single player, TSMC. High bandwidth memory is supplied by only a handful of firms. Nvidia commands 90% of AI data centre GPUs, and its revenue is heavily concentrated in a small group of customers, Microsoft, Amazon, Meta, Alphabet, many of whom are also primary investors in the AI labs driving the latest wave of demand. This is not a broad, diffuse network. It is a tightly interdependent system.

Echoes of Past

We have seen versions of this structure before. In the late 1990s, during the telecom and fibre boom, carriers borrowed heavily to build long haul and metropolitan region networks. Equipment vendors such as Lucent and Nortel did not just sell the hardware. They became financiers, extending generous terms and credit to their customers, telecom carriers such as WorldCom and Global Crossing. Capital markets funded both sides of the equation.

The result was a spectacular overbuild. By estimates, more than 80% of installed long haul fibre remained dark years after the cycle turned. When demand and funding failed to live up to the story, the system could not support itself. Carriers defaulted. WorldCom and Global Crossing went bankrupt. Vendors were forced to write down both receivables and assets, even as their reported growth during the boom had looked impressive.

The parallel or comparison with AI is not exact. AI is a broader and more flexible computing platform than long distance telecom. But the rhyme is hard to ignore. Concentrated counterparties, vendor supported demand, and a system where funding conditions become a critical input into the growth story.

Implications

From a distance, the AI buildout still appears as a powerful and justified growth story. For firms sitting close to the AI ecosystem, Nvidia, Microsoft, Amazon, revenues are expanding rapidly, margins are strong, and the strategic importance of the technology is clear.

Beneath the surface, three features stand out.

First, elements of earnings quality are tied to a relatively closed loop of capital, contracts and counterparties. Growth is not purely a function of broad based adoption. It also reflects continued investment within a concentrated ecosystem.

Second, the economics of the underlying infrastructure require sustained, high levels of reinvestment. The short effective life of AI hardware turns what might appear to be a one time buildout into an ongoing capital cycle.

Third, both supply and demand are highly concentrated. A small number of companies sit at the centre of funding, production and consumption, increasing the system’s sensitivity to changes in capital allocation, regulation or technology.

None of this invalidates the importance of AI. The technology may well deliver substantial long term value. But whether today’s AI infrastructure trade reflects durable, independent demand or a more reflexive system supported by concentrated capital flows will ultimately depend on the top of the cake. Until end users generate enough revenue to fund the capital needs of the stack on their own, the middle layers will remain heavily reliant on the same loop of capital that has powered the boom so far.

Our way of investing makes us cautious about having positions in the stocks of the current beneficiaries and drivers of the AI revolution at current valuations. Calling it a bubble is always risky when the bubble is happening because bubbles can become bigger for unpredictable length of time before they burst. The question is not about the power and value AI is bringing, and will bring to the world, it is whether the speed at which it happens can match the timelines of the capital flowing into it.

The circular nature of the capital flows is not hidden, the deep pockets of these players are deeper than what we can fathom, but pockets are not limitless and nor is the patience of the capital market. Investors must recognize their limitations when making any decisions about investing in the AI trade because history tells us that when the music stops it is the retail investors who are left high and dry.

In contrast, money is flowing out of most other sectors and markets, making them cheap and attractive opportunities. While in the short run the market can behave as a voting machine, it eventually behaves as a weighing machine in the long run. An intelligent investor would be advised on looking for such opportunities where the risk to reward ratio is significantly more favourable.

Explore now and research companies such as:

Reliance Industries Tata Consultancy Services

HDFC Bank Tata Motors State Bank of India

Or simply search for any company you wish to analyse and get the information you need — all in one place.

Already have an account? Log in

Want complete access

to this story?

Register Now For Free!

Also get more expert insights, QVPT ratings of 3500+ stocks, Stocks

Screener and much more on Registering.

Comment Your Thoughts: